|

| Cartoon from 1864 poking fun at politicians and greenbacks (source and explanation) |

{kind=link}

During the greenback era, the Union government issued irredeemable paper money to help pay for its war against the Confederates. What many people don't realize is that there were actually two different strains of greenbacks—those printed before March 1862 and those printed after. Although these two strains had only slightly different properties, they were not fungible with each other and would go on to have drastically different values in the marketplace. Looking at the respective properties of each type gives some insights a thorny problem: why do colored bits of paper money have value?

One classic explanation for the value of fiat money is so-called 'tax-backing.' If the government stipulates that taxes must be paid using government-issued chits of paper, then that will be sufficient to give those chits a positive value. Back in 1910 economist Philip Wicksteed was one of the first economists to champion this explanation:

The Government, then, levying taxes upon the community, may say: "I shall take from you, in proportion to your resources, as a tribute to public expenses, the value of so much gold. You may pay it to me in actual metallic gold or you may pay it to me in anything which I choose to accept in lieu of the gold. If you do not give it me I shall take it from you, in gold or any other such articles as I can find, and which would serve my purpose, to the value of the gold. But if you can give me a piece of paper, of my own issue, to the face value of the gold that I am entitled to claim of you, I will accept that in payment." Now, as these demands of the Government are recurrent, there will always be a set of persons to whom the Government paper stamped with a unit weight of gold is actually equivalent to that weight of gold itself, because it will secure immunity from requisitions to the exact extent to which the gold would secure it. - The Common Sense of Political Economy, Book II Ch 7The idea that a tax obligation can be the basis of money, or what Randall Wray has termed twintopt, is at the core of modern monetary theory, or MMT.

Let's see how the tax backing theory holds up during the greenback period. To set the context, South Carolina had seceded from the Union in December 1860, soon followed by ten other states. Hostilities between the Union and newly-formed Confederate states began in April 1861. To help fund the Union side of the war effort, an initial $50 million issue of greenbacks was authorized in July. This was to be the first government paper money emitted since the Second Bank of the United States had been wound up.

The act ruled that these notes were to be redeemable on demand in gold, a promise that was also inscribed on the face of each note (see below). They thus earned the nickname demand notes. This promise meant that, at the outset at least, their price could not deviate from par since any movement above or below their gold value would be arbitraged away. When redemption was rescinded a few months later on December 30, 1861, demand notes began to trade at a 1-2% discount to their face value in gold.

Greenbacks were introduced in 1861. Note the progression from the first issue—ie 'demand notes'—to the second in 1862—'legal tender notes'. pic.twitter.com/ELnSg3QRtB— JP Koning (@jp_koning) October 10, 2017

The second vintage of greenbacks, known as legal tender notes, was authorized two months later by the Legal Tender Act of February 25, 1862. This act provided for an issue of $150 million, much larger than the first vintage. One novelty is that the second batch of notes was declared legal tender, which meant that a creditor could not refuse to receive them at par in discharge of a debt. The legal tender property was extended to demand notes in March 1862. The second vintage of notes was also irredeemable, putting them on the same basis as the demand notes, which became irredeemable at the end of 1861.

What distinguished legal tender notes from demand notes? As the tweet above shows, the two vintages had visible differences—unlike demand notes, legal tender note did not have the promise to redeem on demand printed on their face. Demand notes also had an extra promise inscribed on them: "receivable in payment of all public dues". What this meant in practice is that the government accepted demand notes in payment for all taxes, including customs dues, whereas legal tender notes were only receivable in a narrow range of internal revenue taxes—and not for customs dues—which at the time made up the majority of Union tax revenues.

Receivability for customs dues was an important point of departure between demand notes and legal tender notes. Duties were priced in gold and could also be discharged with gold coins. So if an importer was on the hook for $x in custom duties, they could certainly scrounge up $x in gold coin to get rid of the obligation, but $x in demand notes would be sufficient to "secure immunity" from the tax. Not so with legal tender notes.

A given importer might only need a small portion of the demand notes in his possession to pay customs duties. Anything above that amount would be worth less than their face value to him, since gold—not demand notes—was necessary to buy goods internationally. However, if that importer could find other importers who were themselves under obligation to pay customs duties, and who would therefore value his remaining stash of demand notes for their tax receivability, then he might sell them his remaining demand notes at a price quite close to the value of gold coins.

So all that was needed to have irredeemable demand notes trade near the value of gold was a permanent market of tax payers who demanded those notes, and a flow of new notes that did not exceed the rate of drainage provided by the tax outlet. After all, if the supply of notes overwhelmed the amount of tax that needed to be paid, then notes would accumulate in importers pockets with no one willing to bid for them. Once everyone's taxes had all been paid up, demand notes would trade at a discount to gold coins.

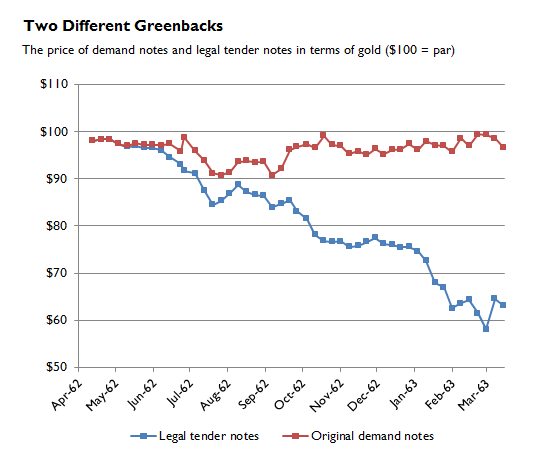

Tax receivability was successful in keeping the value of demand notes close to their gold value. The chart below shows the price of both demand notes and legal tender notes relative to gold through 1862-63. Demand notes never fell to more than a 10¢ discount relative to gold coin. Calomiris blames this discount on the risk that receivability for customs duties would be revoked by the government before notes had been paid in.

Legal tender notes, however, fell to an ever larger discount relative to both gold coin and demand notes, reaching a 40¢ discount by March 1863. While legal tender notes were receivable for domestic taxes, these taxes did not account for a very large share of government revenues. Nor were these taxes priced in gold. Which meant that, unlike demand notes, legal tender notes were not benchmarked to some real good or price index.

So what, if anything, determined the price of legal tender notes? Here I'll introduce another theory for the value of money; the metallist viewpoint. Rather than tax receivability driving a currency's value, a metallist looks to the currency's intrinsic value. When banknotes are fully redeemable, their intrinsic value is determined by the underlying gold on which the note is a claim, the value of which is set in the market for precious metals in technology and the arts.

In the case of legal tender notes, which were no longer redeemable, the realization of intrinsic value had only been delayed to some future point in time when gold convertibility would be re-adopted. This eventual re-mooring date was in turn a function of the Union government's ability to win the war, among other factors. According to this theory, the steady decline in the gold value of legal tender notes in the chart above can be blamed on the realization by the public that the war would last much longer than most originally thought, pushing the re-mooring date ever further into the future.

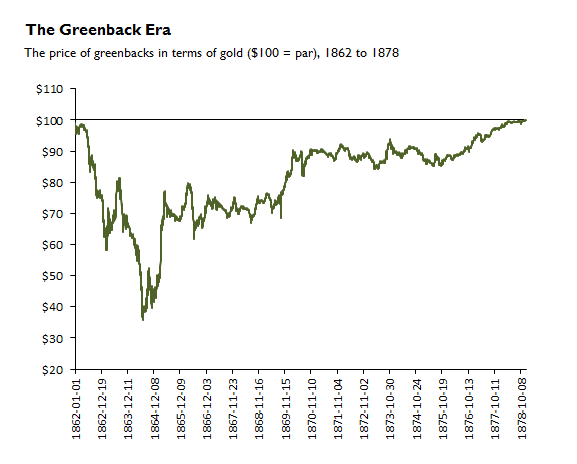

While the 1861 issue of demand notes had all been bought back and cancelled by the government by mid-1863, greenbacks remained outstanding even after the war had been won. Their discount to gold continued to widen till July 1864 at which point their price steadily rose. See the chart below. The steady return to par probably can't be explained by the tax-backing theory. Improved odds that the government's fiscal situation would allow it to resume gold convertibility—an event that finally occurred in 1879—is a better explanation. There have been a few interesting accounts written about the value of greenbacks over the full 1862-1879 period, including Wesley Clair Mitchell's A History of the Greenbacks in 1903, but also more recent contributions here (Calomiris), here (Smith & Smith) and here (Willard et al).

In sum, the U.S. government was issuing three non-fungible currencies by 1862. Coins and legal tender notes operated under the principles of a metallic money whereas the third, demand notes, seems to have been a purely tax-driven money as described by Wicksteed. So what about a modern dollar note? Is a Federal Reserve note like an 1861 demand note and mostly tax-driven, or like legal-tender notes and operating on a metallic basis?

I'm not entirely sure, but my guess is that it is a messy combination of both. When it comes to money, I'm not a believer in any one theory. Although the odds of a future return to the old 1972 gold redemption rule of 0.024 ounces per dollar is non-existent, the metallic explanation for the dollar's value continues to be relevant. Instead of redeeming currency with fixed amounts of metal as in days of yore, modern central banks repurchase notes with financial assets held in their vault in a manner that is consistent with hitting an inflation target. This is very much like 1800s-style metallism, except with an ever-shrinking CPI basket in the place of a fixed amount of gold.

Sources:

Wesley Clair Mitchell, A History of the Greenbacks

PS: I recently started a discussion board here. Feel free to bring up topics not covered on my more recent blog posts, suggest posts, or discuss ideas that appear on my Twitter feed. I don't like Twitter for long-form discussion; I'd much rather divert them to the board.

PPS: Nathan Tankus responds here.

Were they acceptable for state taxes, and being legal tender, were they acceptable for private debts, and at face or market value? It seems counterintuitive to be deemed legal tender without a set value since anyone not wishing to accept them could just set a below market value on them, rejecting their tender.

ReplyDeleteThey were receivable for federal taxes--not sure about state taxes. And as legal tender, a $10 greenback would discharge any $10 debt. Californians and Oregonians did indeed pass greenbacks at their market value, effectively ignoring legal tender laws. But in the rest of the U.S. this was not the case.

DeleteTwo things:

ReplyDelete1)The picture of the 1862 note looks to me like the note promised $1, payable in gold at the treasury, but it's hard to read and I don't see where it says "legal tender". If that's the case, then it's offering future gold convertibility, (probably at the end of the war, like the confederate dollars did).

2) Chartalists like Randall Wray assert that taxes create, or add to, the demand for dollar notes. The backing theory is different, as it asserts that taxes provide asset backing for the dollar notes. So the Chartalists would explain the value of paper money by drawing money supply and money demand curves, while backing theorists would explain the value of the dollar by writing down balance sheets.

there is no neo-chartalist who would set out to draw money supply and money demand curves

DeleteHi Mike:

Delete1) Check out the back of an 1862 note. You'll see the legal tender stipulation:

https://upload.wikimedia.org/wikipedia/commons/7/78/US-%241-LT-1862-Fr-16c.jpg

2) Isn't tax receivability just one of the many channels of reflux?

Hi jp

ReplyDeleteYes, taxes provide a channel of reflux, or we could also say that taxes provide a means of convertibility. But a money issuer can only maintain convertibility if it's assets are adequate to back its money. so backing is that main thing, and convertibility is secondary

Then why did the value of demand notes and legal tender notes diverge?

DeleteSome sort of backing theory explains the value of legal tender notes--i.e. the ability of the US government to restore convertibility at some point in the future. Demand notes were emitted by the same issuer, and therefore had the exact same backing as legal tender notes, yet they traded at a large premium to legal tender. Because the only difference between the two vintages was that the tax receivability reflux channel was open in the case of demand notes, then that must mean that reflux is not secondary, but is at least on par with backing.

A note that is tax convertible immediately will naturally be worth more than a note that promises to be convertible when the war ends in a few years. That explains the divergence.

DeleteAs for the relative importance of reflux vs backing, reflux is only possible if backing is adequate. If a note promises to be convertible into 1 oz of silver, but the note issuer only has enough assets to pay out 1/2 oz per note, then the note will be worth 1/2 oz, and backing trumps reflux.

"A note that is tax convertible immediately will naturally be worth more than a note that promises to be convertible when the war ends in a few years. That explains the divergence."

DeleteOk, we agree.

If a government says that a $1 demand note will relieve a taxpayer of the obligation to pay x gold ounces worth of taxes, then won't that demand note be worth x gold ounces irrespective of what assets the government has in its vaults?

Traditional bank notes have value because of what their issuer can PAY OUT. Tax-backed notes have value because of what their issuer can TAKE AWAY. If a government issued a gold convertible dollar note, declared it convertible for 1 oz, but only had 1/2 oz worth of assets to back that note, then the dollar note would be worth 1/2 oz.

DeleteSimilarly, if a government issues a tax convertible dollar note, declares it to be tax convertible for 1 oz, but the present value of all of the government's "taxes receivable" is only 1/2 oz, then the dollar note will be worth 1/2 oz.

So taxes receivable is an asset, and this asset backs tax-convertible notes? I suppose that's one way of thinking about it.

DeleteTaxes receivable is a very convenient asset for the government to have on its balance sheet. They can just mark it up by fiat. Unlike, say, gold which can't be manufactured out of nothing.

Convenient in the sense that it's hard to quantify, so a backing theorist could claim, for example, that inflation happened because the government's tax-collecting ability had fallen, and nobody could convincingly dispute it. But the idea makes sense: Countries whose assets evaporate tend to see more than their share of inflation, and the loss of assets is partly the result of a loss of the ability to collect taxes.

DeleteI first started thinking this way after studying the Massachusetts paper shillings of 1690, which were issued when Mass. had no visible assets except their (shaky) ability to collect future taxes.

Ah, ok. I may have been thinking about it wrong. A government might jot down a $40 tax receivable on the asset side of its balance sheet, but the true value of that asset is conditioned by the government's ability to collect the tax, which as you say could be shaky. So a $1 tax convertible note might be worth less than par because taxes are so easy to evade, so notes just aren't that useful?

DeleteCorrect, but I don't see your meaning when you say notes aren't that useful.

DeleteWhy bother trying to get your hands on notes in order to discharge a tax you owe to the government, if the tax is unlikely to be enforced?

DeleteYep; got it.

DeleteI blogged on this post here: http://www.nathantankus.com/notes/an-example-of-tax-driven-money-during-the-greenback-era-a-comment

ReplyDeletehere's a sample paragraph below:

"The most obvious point I would make is the one associated with my project- antebellum bank notes are themselves a clear example of tax driven money. I don’t want to dig up my sources here (I’m through about ⅓ of the tax receivability laws of each state and have been stuck there for a while) but you can check out Bray hammond’s classic in the field for some details. In my view american history is rife with clear examples of tax driven money which shouldn’t be surprising because I’m a committed neo-chartalist. You can also check out my columns related to american money before the revolutionary war here. An ancillary point here is that it's inaccurate to say that Greenbacks were “the first government paper money emitted since the Second Bank of the United States had been wound up”. Treasury notes, which were tax receivable, were issued multiple times since the second bank lost its federal charter, most notably during the Mexican-American war"

Great, I'm heading over to read it right now.

DeleteOn the bits you mention here, weren't antebellum banknotes (unlike demand notes) redeemable in specie, and didn't they trade close to their par redemption value?

Did the treasury notes you mention circulate from hand to hand, like greenbacks did? Usually interest-paying paper never succeeds as a generally accepted medium of exchange because of the awkwardness of computing accrued interest. I am pretty sure I am right to say that greenbacks were the first non-interest paying government IOU (and therefore the first generally-accepted medium of exchange) since the Second Bank of the United States, no?

Nathan:

DeleteHere's what Wray said:

"When it comes to the state’s ability to issue IOU (whether currency, central bank reserves, or treasury securities), what matters again is acceptability on the demand side. As a sovereign power, however, the state can mandate at least some demand for its IOUs by imposing obligations that must be paid in the state’s currency. Beyond that, by sitting at the apex of the “money pyramid,” the state’s IOUs are demanded for clearing purposes and also for reserves of the most liquid assets. We conclude, again, that the constraint on the state’s ability to issue its IOUs comes mostly from the demand side."

So, while he doesn't explicitly draw the money supply and money demand curves, he clearly thinks of the value of money as being determined by money supply and money demand, and money demand is driven partly by taxation.

re: antebellum banknotes- some carried the promise of being redeemable in specie, some didn't. there were also suspension periods where redemption was delayed indefinitely.

Deletewithin a state many state chartered banknotes traded near redemption value. however, if their value was primarily being driven by the possibility of redemption. they wouldn't be anywhere near par. even a bank in your state might be prohibitively expensive to travel to. it was also certainly very possible they wouldn't have specie on hand, would refuse you in some way or the bank would collapse. near or at par was preserved because they were receivable in payment of taxes and receivable in payment of private debts as long as, legally speaking, the promise of redemption remained. they also had the insurance value of being receivable in payment of taxes in case there was a mass specie conversion suspension.

some treasury notes circulated hand to hand, some didn't and that line also was created by whether they paid high interest or not. there were some "small denomination" ones and some larger ones. I plan on looking at the denominational structure of the latter issuances but i suspect the latter ones were similar to the war of 1812 issuances. it certainly is misleading to draw a line from continentals, through BUS notes and to greenbacks without mentioning treasury notes.

Interesting about antebellum notes. What about all the note discounts catalogued by the various banknote reporters? Say a bank note reporter tracks note discounts in Philadelphia. Are you saying that notes issued by a bank in Pittsburgh were not discounted in Philadelphia because both cities were in the same state, and because the state government would accept both at par to pay taxes? And that notes issued by a bank in New York were discounted in Philly, even though New York was closer to Philly than Pittsburgh?

DeleteAbout treasury notes, I dunno. If you can show that they regularly circulated from hand-to-hand, and not just between those dealing in financial markets as a form of collateral, but also between small time merchants, wholesalers, and even consumers then I'd buy it.

Come down to new york, I've looked at bank note reporters in person at the American Numismatic Society :)

DeleteI said "traded near redemption value". The exceptions were when there was a mass suspension and "pennsylvania money" fell to a discount relative to gold or silver (whichever one was the defacto peg towards) or when the discount reflected the uncertainty that that bank would continue specie payments/would fail all together.

and yes its clear that distance discounts where more pronounced between states then within states. some states also had requirements (pennsylvania is actually a strong example) that each chartered bank had to accept others in payment of debts. the more general requirement was that if you paid out a note at par you need to receive it at par.

Really interesting stuff. Make sure you send me some material when you're done, curious to see what you find. I'd imagine that it's going to be tough slog going through old edicts and scanning through bank note reporters. Hopefully someone has already digitized all the note discount data?

DeleteI don't think we have a good data set of the note discount data but i have to look around more. all the major libraries like the ANS are in the process of digitizing their collections.

Deleteall (okay, most) of the laws are digitized so that's an easier time. i'm about a third of the way through. hoping to cut out a big chunk of time in the spring to finish a draft of the tax receivability element of this project.

> JP

DeleteHow does the value of the note fluctuate in dollars when the note is itself a dollar. What are you using as the dollar reference , is it weight of a silver dollar coin. And what is defined as the convertibility of a note to gold is it weight of gold or dollar value of gold.

The price of a $1 greenback is relative to a $1 gold coin. Notes are convertible into an equivalent amount of gold coin, so a $5 note should get you $5 in coin.

DeleteAs it is gold coin , there is a risk that the issuer will not be able to afford to honour the convertibility. And so, fundamentally, the credibility of Both Greenback notes is based on the same thing, the good condition of the issuer.

Delete"... modern central banks repurchase notes with financial assets held in their vault in a manner that is consistent with hitting an inflation target. This is very much like 1800s-style metallism, except with an ever-shrinking CPI basket ..."

ReplyDeleteWhat the CB is doing there is regulating the growth of commercial bank deposits. And so the value of CB bank notes is the value of commercial bank deposits, the value of which is the value of economic resources sold when honouring commercial bank loan contracts.

"... the metallic explanation for the dollar's value continues to be relevant. Instead of redeeming currency with fixed amounts of metal as in days of yore, modern central banks repurchase notes with financial assets held in their vault in a manner that is consistent with hitting an inflation target."

ReplyDeleteIsn't this an example of circular reasoning? If I am not mistaken, the Fed's balance sheet consists mainly of financial assets that pay a stream of USD. So the USDs issued by the Fed have value because they are backed by financial assets paying a stream of USD issued by the Fed?

There is definitely some circularity here. Maybe that's why central banks still like to hold a bit of gold.

DeleteDuring the financial crisis, some banks strengthened their balance sheet by giving loans to investors who then used these loans to buy shares in the bank. It's not exactly the same thing, but isn't accepting that financial assets paying USD issued by the central bank can meaningfully back the value of those same USD somewhat akin to accepting that the aforementioned type loan/equity transaction can meaningfully improve the financial strength of a commercial bank?

ReplyDeleteActually that aforementioned loan/equity arrangement can improve the financial strength of a commercial bank as the loan is a new asset of the bank.

DeleteLet me add some more detail, to get closer to the central bank case. Suppose I am the investor. My only asset is the shares in the bank. My only liability is the loan to the bank. Would you still argue that in this case the loan/equity transaction somehow improves the financial strength of the bank, that it somehow backs the value of its equity? I would think not. Maybe I am wrong, but I think this is very similar to the idea that the value of USD issued by the Fed can somehow be backed by a financial asset paying a stream of those very same USD.

DeleteIf that was your only asset then you would honour the loan by selling the position of shareholder to a deposit holder, thus reducing the banks liabilities.

DeleteTo see how financial assets have any value you have to look beyond financial assets , to what they represent. It is the value of commercial bank deposits, the value of which is the value of economic resources sold when honouring commercial bank loan contracts. The value of A USD issued by the Fed is maintained by controlling the growth of commercial bank deposits, by intervening in interbank market for dollars with bond sales.

"...but isn't accepting that financial assets paying USD issued by the central bank can meaningfully back the value of those same USD..."

DeleteYes, assets like bonds that pay out out in the very same currency they are supposed to be backing are not great assets because of the circularity problem.

But as long inflation expectations are well anchored than bonds will suffice for fine tuning. If things suddenly get bad and the price level starts to shoot up, the central bank needs to mobilize a real resource like gold that does not lose its value to inflation. Remember too that a central bank is owned by the government, which can extract a real amount of resources from its population via taxes and transfer that to the central bank for additional firepower.

Just the threat of being able to draw on this resource is often enough to keep things in check. Once these lines of defense break down we get something like present day Zimbabwe.

Sorry for this long reply. It didn't have the time to make it shorter.

Delete"Yes, assets like bonds that pay out out in the very same currency they are supposed to be backing are not great assets because of the circularity problem."

In financial markets, a situation where an asset's value goes to zero at precisely the moment when you need it to be non-zero is called wrong-way risk. As a rule, one usually does not assign very much value to this kind of protection.

"But as long as inflation expectations are well anchored than bonds will suffice for fine tuning."

Isn't the use of bonds for fine-tuning based on the idea that the cb can affect inflation through the interest-rate channel? The way I understand it, the bonds on the Fed's balance sheet are there because the Fed thought that buying these bonds would put downward pressure on interest rates, which in turn would stimulate credit creation, which in turn would stimulate demand. I don't think they are there because the Fed thought that the USD was insufficiently backed by financial assets and that therefore it needed to add some bonds to its balance sheet.

Is what you are saying about the real resources and Zimbabwe that, in the absence of a robust domestic economy and a strong and stable domestic government, the central bank needs gold (and perhaps also foreign-currency reserves or foreign-currency bonds) on its balance sheet to back up the domestic currency? If so, then I have understood you correctly and would tend to agree.

Looking at the Fed's balance sheet today, I see the asset side consists mainly of treasuries and mortgage-backed securities. I don't think the treasure do much, if anything, to support the value of the USD because, as you rightly mention, the cb is under control of the government and so there is this whole circularity thing going on. It reminds me a bit of this company (Hampton Creek?) trying to shore up its business by sending employees out to supermarkts to buy its own produce.

I do think that the mortgage-backed securities support the value of the USD, not by being on the Fed's balance sheet, but by the mere fact that they exist. The fact that these mbs's exists means that there are private-sector liabilities payable in USD. The existence of these private-sector liabalities creates private-sector demand for USD which will act as a support for its value. I suppose these private-sector liabilities were entered into voluntarily by the private sector. I guess the whole point of neo-chartalism is that by its power to create liabilities in the currency it issues, the state can create demand for its currency and hence support its value. I do get the impression that it is indeed this power that is the foundation of the value of a currency. All the other effects can leverage and magnify this fundamental value (voluntary liabilities in the currency, network effects etc.), but seem to me not to be the fundamental basis of that value.

"The way I understand it, the bonds on the Fed's balance sheet are there because the Fed thought that buying these bonds would put downward pressure on interest rates, which in turn would stimulate credit creation, which in turn would stimulate demand. I don't think they are there because the Fed thought that the USD was insufficiently backed by financial assets and that therefore it needed to add some bonds to its balance sheet."

DeleteThe central bank buys bonds in order to inject settlement balances into the clearing system, which in turn affects the overnight rate as well as other variables like the price level.

It could of course simply inject settlement balances by crediting them straight to a commercial bank's settlement account ... without getting a bond in return. But the idea is that it is prudent to take some sort of security in case the borrowing bank fails.

And furthermore, if the central bank needs to reduce settlement balances in the future for the purposes of monetary policy, having bonds on hand that can be quickly sold will be the most rapid way of doing so. If it originally expanded by straight up crediting a commercial bank's settlement account, and not via a bond purchase, it would have to shrink the supply of settlements by waiting for those credits to mature, and this might be too unresponsive.

Sounds reasonable to me.

Delete(Previous comment deleted due to too many spelling errors.)

DeleteJP,

I was reading your reply again.

"The central bank buys bonds in order to inject settlement balances into the clearing system, which in turn affects the overnight rate as well as other variables like the price level. "

Is this correct? I thought the objective of QE - which I think is responsible for the majority of bonds on the Fed's balance sheet - was to lower long-term interest rates by driving up bond prices as the effect of overnight rates on long-term rates was thought to be too weak. I was not aware that a shortage of settlement balances was the driver.

Guess I should express myself more clearly. Pre-2009 the objective of bond-transactions was indeed to affect settlement balances, but post 2009 is a different story, or not?

DeleteYep, that's right, different story. In academic speak, the goal of QE was to lever the 'portfolio balance channel.' David Beckworth is good on explaining this:

Deletehttp://macromarketmusings.blogspot.ca/search?q=portfolio+channel

>JP

Deleteyou say that "... modern central banks repurchase notes with financial assets held in their vault in a manner that is consistent with hitting an inflation target."

How exactly does that work , in your view.

My 2 cents.

DeleteThe central bank has a target interbank overnight rate, the rate at which banks lend reserves to each other. Banks need reserves e.g. for payment settlement and in relation to the deposits on their balance sheet (fractional-reserve banking, zero in some countries). If there is an excess of reserves in the system relative to the needs of the banks, this will cause downward pressure on the overnight rate. By selling bonds in exchange for reserves, the central banks drains reserves from the system, thus supporting the overnight rate. If there is a shortage of reserves, there will be upward pressure on the overnight rate. The central bank then injects reserves into the system by buying bonds in exchange for reserves, thereby reducing the upward pressure on the overnight rate. The thinking goes that the level of the overnight rate as well its future evolution influences other rates in the economy - both long-term and short-term - and that this in turn influences economic activity, demand for investment and consumption and hence inflation. Since the introduction of QE, there is a huge excess of reserves in the system. This would cause the overnight rate to drop to zero. Hence the need for the Fed to pay IOER in order to hits its overnight target.

But how do rates influence " economic activity, demand for investment and consumption and hence inflation "

DeleteIn a very indirect and hard-to-predict way in my opinion. I find the mechanics of the relationship between the amount of reserves and short-term rates quite convincing. I think the effect of short-term rates on inflation is highly uncertain. (See also the whole Neo-Fisherite debate.) I have yet to read an explanation of the transmission channel of monetary policy that I find persuasive. I think all these central bankers agonizing over whether and when to hike or cut by 25 bp are engaged in an exercise of futility. Still, they are the experts, they spend all their time thinking about this, so it seems rather presumptuous on my part to think that they don't know what they are doing and I do just because I've read a few blogs.

DeleteI don't see anything I'd disagree with in your October 23, 2017 @ 8:36 AM comment.

DeleteThanks. The 9:08 AM comment is slightly more controversial I should think. :-) I suppose the majority of people who have an opinion on these matters would tend to disagree with me on this. If you - or anyone else here - could point me towards a well-argued case in defense of interest-rate policy, I would be really grateful.

Delete> JP

Deleteyou say that modern central banks repurchase notes with financial assets to, as you say " hitting an inflation target."

How exactly does that work , in your view.

This is going beyond the topic of tax driven money and may be better for the discussion board:

Deletehttp://moneyness.freeforums.net/board/1/general-discussion

The reason these loan/equity transactions were done was that the banks that engaged in this practice were unable to raise capital in the normal way (i.e. without first loaning investors the funds to buy the shares). So in this example, if I had to sell my position, I wouldn't have found any buyers. I am of the opinion that a loan backed only by shares no-one is willing to buy is of little to zero value.

ReplyDeleteAs it stands, I don't agree with your assessment that the value of a USD issued by the Fed is maintained by controlling the growth of commercial bank deposits. However, I do get the impression that we agree on the fact that the value of the USD is not maintained by the value of USD financial assets on the Fed's balance sheet.

The loan isn't backed by shares , its backed by the promise of future payment. A loan that isn't paid isnt worth anything and that applies to all bank assets. The investing shareholder who presents a promise of future payment would have to be credible.

DeleteThe value of a banks liabilities is its assets. And so the CB could be simplified by just discussing the assets, which are mainly Treasury Bonds funded by taxing taxpayers commercial bank accounts, and so it refers to the value of those liabilities and assets and what transactions those assets are honoured with.

"... Treasury Bonds funded by taxing taxpayers commercial bank accounts ..."

DeleteAre you saying that in the US taxes can be paid by commercial banks crediting the treasury's accounts with these commercial banks? That is not how it works in my country. Here, the treasury has an account witht the central bank, and taxes have to be paid in central-bank money into that account.

Hi jaw

DeleteThe small amount of central bank money flows back and forth, reciprocating, between accounts of banks and the Treasury held at the central bank during the day, but at the end of the process the actual tax payments from individuals is from their own commercial bank deposit accounts.

The predominate money in the economy is commercial bank deposit accounts. Central bank money fascinates movements of it between banks. Government taxing and spending starts and terminates in deposit accounts. It is money in deposit accounts that government activity moves around.

"at the end of the process the actual tax payments from individuals is from their own commercial bank deposit accounts"

DeleteSo, to repeat my previous question, are you saying that the US state considers a tax to be paid when its account at a commercial bank is credited by the right amount? If yes, then you are right. If not, then I fail to see how you can say that tax payments are from individuals their own bank deposit account. When I pay may taxes, my bank debits my bank account, the cb debits my bank's cb account and credits the treasury's cb account. Afaik, if my bank has an insufficient balance on its cb account, then the cb will refuse to credit the treasury's cb account, and the state will not consider that my tax has been paid.

https://www.nbb.be/en/about-national-bank/tasks-and-activities/services-state

DeleteThe National Bank is State Cashier.

The National Bank centralises the revenue and expenditure of the federal State in the account maintained by the Belgian Treasury at the National Bank. That account also records the transactions carried out by the National Bank on behalf of the State, as well as the balance of the transactions the Post Office carries out on behalf of the State (e.g. collecting taxes and social security contributions, paying the wages of the federal civil servants,...).

No there is no Treasury account at the commercial bank.

DeleteBut the payments are to and from deposit accounts, facilitated by central bank money movements between reserve accounts.

To illustrate . A banks holding of reserves does not equal its customers deposit accounts, not for a single bank or all banks as a whole. When a tax payer pays a tax their deposit account is debited. Lets say $1000. The recipient of government spending on that day may receive $1000 in government spending. The next day someone else pays tax $1000. and someone the next day receives $1000. Over the year a $Billion dollars may have changed hands. But only $1000 in central bank reserves needed to exist to facilitate the transfers.

At the end of the year the whole of Tax payers have $1Billion less and recipients of government spending have $1Billion more. But only £1000 of CB money existed.

That illustrates how government when it taxes and spends it does so with commercial bank deposits.

I do agree with the broad outline of what you are saying. But I think you leave out some crucial steps. After "When a tax payer pays a tax their deposit account is debited. Lets say $1000.", you should add: "The commercial bank's account at the cb is debited by $1000 and the Treasury's account at the cb is credited by $1000." If the commercial bank has insufficient reserve balances at the cb, and cannot get its hands on reserves in the interbank market, or by using some kind of lending facility from the cb (vs. collateral), then the process ends before it even starts: the tax payer's deposit account at the commercial bank is not debited, the commercial bank's account at the the cb is not debited, the treasury's account at the cb is not credited, the tax has not been paid. I totally agree that there are a lot of flows back and forth with substantial netting at the end of the day, but nett flows are settled in cb money, not in commercial-bank money.

DeleteThis applies also to payments between commercial banks: they are settled in cb money, not in commercial-bank money. At the end of the day if bank A has to receive a payment from bank B, bank A is not content with a statement from bank B that bank B has credited bank A's deposit account. What bank A needs to see is a statement from the cb that it has credited bank A's reserve account for the correct amount.

It seems to me that commercial-bank money has value only to the extent that is convertible one-for-one into cb money, not the other way around. If that convertibility is compromised, then so is the value of the commercial-bank money and we have ourselves a bank run.

Yes when the tax payers deposit account at the bank is debited , so is the banks account at the cb debited , for that transaction.

DeleteBut do you see in the summary of the years taxing and spending it is deposit money that is the money being taxed and spent. Tax payers have less money , recipients have more, but the relatively smaller amount of cb money may be back where it started.

Another example - If the recipient of spending and the tax payer are at the same bank then there is a net change in deposits, but no net change in reserves. In fact banks are becoming more efficient and netting off transactions more nowadays without using CB clearing.

The hypothetical scenario of an instance of non convertibility of a banks commercial bank money into CB money, well that is a hypothetical scenario, it could also be stated the other way round, CB notes would be less liquid and popular if commercial banks refused to accept them , also hypothetical.

But I think the pertinent point here is that commercial bank money is endogenously valuable as each unit of it is backed by a borrowers real obligation stemming from their loan contract to sell something to a deposit holder, that the deposit holder values. The credibility of that overseen by a bank loan officer.

And commercial bank deposit money is the predominant money used in the economy.

"But do you see in the summary of the years taxing and spending it is deposit money that is the money being taxed and spent."

DeleteThe net summary of the years of taxing and spending is the government debt, payable in central-bank money.

"The hypothetical scenario of an instance of non convertibility of a banks commercial bank money into CB money, well that is a hypothetical scenario, it could also be stated the other way round, CB notes would be less liquid and popular if commercial banks refused to accept them , also hypothetical."

Hypothetical? Northern Rock, Landsbanki, Kaupthing, DNS Bank, ... Do you want me to go on?

Take the following example. (from https://en.wikipedia.org/wiki/List_of_bank_runs#2000s)

"On 11 December 2011, a rumor was spread via Twitter that the Swedish banks Swedbank and SEB were having "problems" and there was a lesser hysteria in Latvia. People emptied their accounts, and according to local media there were long lines of people at the cash machines.[27] On December 12 the authorities started an investigation to locate the cause of the rumors, and the spokesman for Swedbank said that the situation seemed to be calming down.[28]"

In cases like this, commercial-bank deposit holders care about one thing only: converting their commercial-bank money into central-bank money (notes and coins) as soon as possible. How many examples do you know of cases where people ran to their local bank in a blind panic to convert notes and coins to commercial-bank deposits for fear that the notes and coins would be worthless and in the expectation that the commercial-bank deposits would retain their value?

"In fact banks are becoming more efficient and netting off transactions more nowadays without using CB clearing."

True, undoubtedly. And how is the amount that is left over after netting settled?

"But I think the pertinent point here is that commercial bank money is endogenously valuable as each unit of it is backed by a borrowers real obligation stemming from their loan contract to sell something to a deposit holder, that the deposit holder values. The credibility of that overseen by a bank loan officer."

I totally agree with this. The commercial-banks assets are there to ensure one-for-one convertibility of commerical-bank money into cb money. Also, a borrower's real obligations have to be settled in central-bank money, no? If I have a payment to make on my loan, and all I have is a deposit account at a failed bank, I don't think whoever I have to make the payment to is going to be very happy if I write him say a cheque on that account. If I pay him in central-bank notes of whatever currency the loan is in, on the other hand, I'm sure he'll have no problem with that.

Yes I have repeatedly noted in the thread that debts between banks are settled in cb money. So no disagreement there.

DeleteBut a borrowers real obligations do not have to be settled in cb money. If they have a current account at the lending bank , as most borrowers do , and they sell something to a fellow deposit holder at the bank , then the loan can be settled. Do you see how commercial banking is endogenous.

What you describe here is netting of liabilities, not settling the residual that cannot be netted.

DeleteYes that is correct and you have repeated the first 16 word sentence of my previous comment.

DeleteIf you say so. Let me continue to draw inspiration from that same comment by paraphrasing the first two sentences of the second paragraph. Real obligations of borrowers do not have to be settled in cb money because offsetting liabilities vis-à-vis the same commercial bank can be netted. I admit to not quite following your logic here.

DeleteI am not sure what particular point we are exploring Here.

DeleteMy original observation was that now, in the contemporary economy, the value of central bank notes is determined by the amount of, and the velocity of, commercial bank deposits.

We arrived at this point precisely because of this - to me rather exotic - observation that the value of treasuries and central-bank notes is somehow determined by the amount of commercial-bank deposits, and also their velocity, apparently. Do you have any arguments to support this observation? Is there any economic school of thought that holds this view? I was trying, in vain so it would seem, to explain why I don't think there is any such causal link running from the amount of commercial-bank deposits to the value of central-bank deposits. My main argument is that we measure the value of commercial-bank deposits by our ability to convert them one-for-one into central-bank money (notes in coins in our case). If what you say is correct than I would think it would be other way around: we would measure the value of central-bank money by our ability to convert it into commercial-bank money. We don't and therefore I think you are mistaken. If you feel there are other relevant arguments that I am not seeing, do not hesitate to share them.

ReplyDeleteOf course I have evidence to support it, it is trivial to do that, it is the interest rate policy of central banks .

DeleteCould you please be a bit more detailed and specific, for the benefit of my education. I fail to see how the interest-rate policy of the central banks proves that "... Treasury Bonds [are]funded by taxing taxpayers commercial bank accounts ..." as you claimed in the comment at the start of this thread.

DeleteMy comment was that now, in the contemporary economy, the value of central bank notes is determined by the amount of, and the velocity of, commercial bank deposits.

DeleteI'm no economist, so maybe I am mistaken, but I do believe that the idea that there is some simple direct link from the amount and/or velocity of monetary aggregates to the value of central-bank notes (which I take here to be the inverse of the price level) is old-style (as in 1970's) monetarism. Afaik central banks gave up trying to control inflation (which I take to be the erosion of the value of central-bank notes) through monetary aggregates a long time ago, for the simple reason that monetary aggregates are essentially all over the place uncontrollable most of the time. Just look at some charts of (the velocity of) USD M1 money stocks on Fred to see what I mean. If you are able to explain the evolution of US CPI by using the evolution of M1 and/or its velocity, you have my full attention. If this is not what you mean by your comment that "the value of central bank notes is determined by the amount of, and the velocity of, commercial bank deposits" then I do apologize but is rather hard to figure out exactly what you mean as you don't provide an awful lot of details with respect to your logic.

DeleteRegardless of the particular dynamics it is still deposits that effect cpi and thus the value of cb notes.

DeleteSo, what is your point exactly? As it stands your statement is too vague to either agree or disagree with.

DeleteJP's post finishes with a reference to metallism and the modern dollar note

Delete"Instead of redeeming currency with fixed amounts of metal as in days of yore, modern central banks repurchase notes with financial assets held in their vault in a manner that is consistent with hitting an inflation target. This is very much like 1800s-style metallism, except with an ever-shrinking CPI basket in the place of a fixed amount of gold. "

I am observing an addition to his point about the Fed and CPI that now in the modern economy that the CB is not aiming at CB notes directly, it is commercial bank deposits, the predominate form of money, that effect the domestic value of the dollar and the value of the CB note stems from that.

Let's t ry to break this down.

Delete1) What exactly do you meand by the dollar?

2) How do commercial bank deposits affect the value of the dollar in your opinion?

3) What is the differcence between a cb note and a dollar and how does the value of a cb note stem from the value of the dollar?

The theme of the post is

Deletequote

"why do colored bits of paper money have value?"

1)The dollar is predominantly commercial bank deposits

2)not making any assumptions about interest rates etc, see above no-one here had an answer, except the fundamental relationship with the value of the goods and services sold by borrowers.

3) The value of the dollar is valued as a basket of Goods , CPI, in JPs thesis above.

Therefore it follow from 3) and 1)

my comment above Oct 27 5.10 am

1) I am assuming that by colored bits of paper money you mean e.g. a 1 USD note in your pocket today. This 1 USD note is central-bank money, not commercial-bank money.

Delete2) So, you say that on the one hand the dollar is predominantly commercial-bank deposits and yet on the other hand you do not want to make any assumptions about how commercial-bank deposits affect the value of the dollar. Surely you can see the logical inconsistency in your statement.

3) Also, when you say commercial-bank deposits, do you mean only domestic dollar deposits or are Eurodollar deposits included as well, and why (not)?

4) The CPI is one way to measure the value the dollar, I'll grant you that. Another way to measure the value of the dollar is by, say, its exchange-rate vs. the Euro. I don't see how 'it' follows from any of this. (It is probably true of course that the Fed is much more concerned about US CPI than about EUR/USD.)

5) Why do colored bits of paper have value? In this post, JP gives a beautiful example of the fact that, in the absence of guaranteed convertibility into some valuable commodity, the ability to pay one's taxes with it seems to be one way to provide a pretty solid foundation for the value of fiat currency. I don't see how one can draw any inferences about the relationship between the value of fiat money and commercial-bank deposits from this post. (I use the term fiat money i.s.o. central-bank money because afaik there was no central bank yet during the civil war.)

You can make the inference from the post because JP uses CPI.

DeleteI gave the definition of the dollar as a response to your "break down". Dollars are predominantly bank deposits and CB notes are of course CB notes and "Exchange rates" - I stipulated the domestic value. I am not complaining but you don't seem to be reading the sequence of posts.

What I am saying is simple - CPI targeting is, if it involves money, must be targeting something about deposits.

Which is relevant to the post as it illustrates how the monetary system has evolved since 1860. That's it really.

I have reread the sequence of posts a few times already. Maybe it's me, but much of what you write seems rather imprecise and confused. I don't know whether I agree or disagree with you, because I don't understand what it is you believe and I don't understand why you believe it.

DeleteIn 1860 the government was not concerned with bank deposits , it was concerned with the Green back value by using for example gold convertibility.

DeleteCPI targeting is not directly targeting the purchasing power of CB notes. It is targeting the purchasing power of commercial bank deposits, and as a consequence the CB note value is maintained . Simple as that.

Simple but wrong.

DeleteThe central bank does a number of things, but not exactly what you describe in your comment. I realize I've said much of this before, but let me try to just summarize it in one comment for ease of reference.

Firstly, monetary policy - CPI targeting as you call it - is concerned with managing the purchasing power of central-bank money.

Secondly, the central bank is involved in managing the convertibility of commercial-bank money - of which there are as many flavours as there are commercial banks - into central-bank money - which you can regard as the purchasing power of commercial-bank money if you like - through its capacity as the regulator of commercial banks, i.e. by imposing capital and liquidity ratios on commercial banks and ensuring that these ratios are respected.

Thirdly, the central bank ensures the smooth execution of large-value interbank payments (FedWire in the US, Target in EUR zone).

In normal times, the central bank is so successful at the latter two tasks, that people like you and me can safely disregard the difference between central-bank money and commercial-bank money. In times of stress, the difference between central-bank money and commercial-bank money and the fact that there are as many flavours of commercial-bank moneys as there are commercial banks becomes apparent. The crowds of customers queueing up outside their local branch in order to convert as much of their commercial-bank money into central-bank money is evidence of this.

Based on previous experience I doubt any of this will convince you. Likewise, you really have to do better than a few short sentences of unsubstantiated - and, to my mind, mostly wrong - assertions if you want to prove the point you are trying to make.

If there is any point on which you would like me to elaborate, feel free to ask and I'll try my best.

In the mean time, I advise you to have a look at Perry Mehrling's Money and Banking course. The course notes can be found on his website (http://www.perrymehrling.com/#). Videos of his lectures can be found on youtube. I find his course is an excellent resource, and I'm sure it can clear up a lot of the confusion you have.

Just to add one more thing. I am not denying that there is a link between credit creation, the amount of commercial-bank deposits, economic activity, the balance between supply and demand, the price level, and hence the value of central-bank money. However, you seem to infer not only correlation, but also very strong causation, and in doing so you seem to get the direction of the causation the wrong way around.

DeleteFirst, in the overview of the causality leading to CB money quantity and banknote quantity, from monetary policy and commercial bank activity, using the operational reality of the banking system, the monetary system. - The CB does not directly set the quantity of CB reserves or banknotes. They are both a product of commercial bank activity. The CB has an interest rate target for CB money. The quantity is a function of what is required by commercial banks , and the CB target interest rate for reserves. The requirement of reserves by commercial banks for clearing deposit transfers, deposits produced by commercial bank loans. If the interbank rate goes up the CB will conduct Open Market Operations and produce more reserves to clear the transactions at the target rate. From that process it is seen that the causality is from deposits to reserves.

DeleteThe number of CB notes produced is the quantity requested by commercial bank customers. The customer requests the notes and then the commercial bank places and order with the CB that some of its reserves , CB money held at the CB, produced by the above process, are converted to notes, which would be then be printed if required to meet demand, and delivered to the bank and its customers. And so again the causality is from deposits to reserves.

These two operational realities combined , can be considered with CPI and monetary policy, and the value of deposits and CB notes.

The target of the CBs monetary policy cannot be CB notes as their quantity is not a CB policy , it is not something they control. People dont spend CB money, they spend deposits. They dont have access to CB accounts, and the notes that they do spend are derived from their holding of commercial bank money in deposit accounts. Deposit money that is produced endogenously by banks and their customers. The deposit holder requests CB notes and then spends their deposits using CB notes. More deposits leads to more notes. Again here the causality is seen to be from deposits to CB notes. The monetary policy is targeting the purchasing power of commercial bank deposits, and as a consequence the CB note value is maintained.

Much of what you write about cb operations, the elasticity of central-bank reserves etc. seems correct to me. However, I don't see how you can arrive at the following conclusion: "The monetary policy is targeting the purchasing power of commercial bank deposits, , and as a consequence the CB note value is maintained." Unless I misunderstand what you mean by that sentence. Do you mean by monetary policy targeting the evolution of the CPI (inflation) through the level of interest rates?

DeleteOk. Let's try to find something we agree on. Would you agree that there are as many flavors of commercial-bank money as there are commercial banks, that a 10000 USD in a deposit account at JPMorgan Chase Bank is not exactly the same as 10000 USD deposit at Salem Five Cents Savings Bank?

DeleteIf money is a promise to deliver goods of equal value in future, then the value of that promise is my trust that the promise will be honoured. As the biggest single issuer of promises, a government can offer an insurance scheme to augment the public's trust and thereby the value of its (and others') promises. That insurance scheme could be (limited) convertibility into a specific good, say gold. It comes at a cost, though. Namely that of the gold it takes to keep it going. Unless, of course, government happens to own the gold mines. There is also a drawback to such an insurance augmented monetary setup. The value of money is always defined in reference to that one good the insurer offers conversion into. That is particularly problematic if the value of that one good in relation to a basket of important consumer goods fluctuates strongly. So a wheat standard in a simple agrarian economy makes much more sense than a gold standard in a modern, diversified economy.

ReplyDelete"So a wheat standard in a simple agrarian economy makes much more sense than a gold standard in a modern, diversified economy."

DeleteRather than wheat or gold , CPI makes sense in the modern, diversified economy.

Greenbacks were "irredeemable paper money"?? A total oxymoron. After that I could read no further, what would be the point? Dude does not understand money. And it wasn't tax driven money, it was war driven money. Seems the only time we get publicly issued debt-free money is when the nation needs to defend itself against the bankers. Coxey's Army and the whole progressive populist movement of the day wanted more Greenbacks issued for schools, roads, utilities etc. promoting the general welfare which is our government's ignored mandate. They tried to get the Greenbacks out of circulation by offering gold for them and still the people would not do it. I can only assume this is banker backed propaganda or just more monetary ignorance.

ReplyDelete